Market failure: Externalities

[This essay is intended for students in my law and economics and my microeconomics class (for law students). Read this essay one time through, ignoring the queries that are interspersed. Go back to the queries after you feel you have understood the essay. The queries test whether you have understood enough to develop a richer understanding of the topic of the essay (externalities). These instructions will also apply to future essays.

I have bolded certain words. These are terms that you should know going forward. If you do not understand them, ask your favorite foundational AI model about them.

I will post the python notebook that generates all the figures in this essay in case you are interested in reproducing them.]

A critical assumption behind the claim that equilibrium prices and quantity in a free market equilibrium yield efficient outcomes is that demand and supply curves reflect social marginal values and social marginal costs. When those assumptions do not hold, e.g., when there are externalities, the market equilibrium may be inefficient. Moreover, the very government interventions—taxes and quantity regulations—that I said would cause market failure in a prior essay, might correct market failure in the presence of externalities. In this essay I explore these issues.

Before we begin, we have to explain what we mean when we say the private demand or supply does not equal social marginal value (demand) or social marginal cost (supply) and why that matters.

To say that private demand does not equal social demand, that means that there is some value that flows from a given consumer purchasing a good that is not captured by that consumer’s willingness to pay for that good. It could be that my buying a drum set hurts you (because of noise), or that I do not fully appreciate the harm (to my future self) of drinking a Manhattan when I get home from work. The former is sometimes called an externality, and the latter an internality. I will unpack externalities in a moment. And I leave internalities for another day. I gave examples where private marginal value is higher than actual social marginal value. But one can find cases where private value is lower than social value. Analogously, private supply does not equal social supply when producing a good has costs or benefits across society that are not captured by the costs that producers of the good face.

The reason market performance suffers when private demand and supply do not equal their social analogues is that a market sets price and thus quantity based on the behavior of market participants, not all of society. Market purchasers comprise private demand. Market sellers private supply. In other words, a market sets price and quantity based on private demand and supply.

What is an externality?

One reason—perhaps the main reason—private demand or supply might not equal social demand or supply, respectively, is that there are externalities. What are externalities?

Before we define externalities, we need to define an external effect. An external effect exists when person A’s behavior, situation or utility has an impact on person B’s utility or happiness. This could be a positive effect or negative effect. For example, my wiping the chalkboard after teaching my class has a positive effect on the utility of the teacher that next uses my class. My lighting a cigarette in class, by contrast, would have a negative effect on the students in my class who find smoking distasteful. The external effect may flow from person A’s situation or utility, not just her behavior. If I learn that a friend of mine has cancer, I feel bad because I sympathize, even though their behavior did not change.

Note that an external effect is not an externality in the colloquial or legal sense. A legal externality is when A has an external effect on B and B has the legal right to not be affected by A in that way. Our colloquial use of externalities is when A has an external effect on B and social norms state that B has a right or privilege to not be affected by A in that way. An external effect can exist regardless of who has a right or is privileged by norms. Let me give an example. Suppose that you and I are roommates. I like to smoke, you like a smoke-free environment. If the law gave me a right to smoke, and the law in 1980 did, then my smoking would not have a negative legal externality on you. If social norms did the same thing, and in the 1960s social norms did, we would not colloquially say my smoking has an externality on you. But if the law or norms changed, so that smoking was frowned upon, we would say that my smoking has a negative externality on you.

Why do we draw a distinction between external effects and externalities? Because it can be hard to imagine that today’s rules were not always the rules. There was a time when it was fine to smoke indoors, now it is not. The external effects on you were the same in the past and now. But the externality changed. (We will expand on the dichotomy between external effects and externality when we discuss the Coase Theorem.) For the purposes of markets, however, what matters is external effects, because they do not depend on legality or norms. All that matters is my preference to smoke and your preference to be free from smoke.1

Going forward we would ideally use the word external effect. But the reality is that economists often use the term externality in place of the term external effect. So we will do the same. However, when we use the term in economics, what we really mean is external effect. It does not matter what the law or norms are, holding our individual preferences constant. All that we care about is that one person’s consumption affects another person’s utility.

Pecuniary externalities

One externality that is often confusing to new students of economics is that shifts in the demand or supply curve will change market prices and thus consumer surplus, i.e., markets cause external effects. For example, if many new purchasers enter the market for a particular good (or existing purchasers experience a rise in income, the good is a normal good), the demand curve shifts out. This causes the equilibrium price to rise. That, in turn, is a negative externality on other purchasers, who see lower consumer surplus. This dynamic is confusing because above we proposed that externalities may cause markets to be inefficient, but in an earlier essay we explained how a market’s price response to changes in demand or supply is a reallocation that maximizes surplus.

We can break this Gordian knot by defining something called a pecuniary externality and clarifying that only non-pecuniary externalities cause market failure. A pecuniary externality is one where the market demand and supply reflects all social marginal value and marginal cost, respectively, even though we may observe market dynamics having external effects. For example, if income causes demand to shift out and this increases equilibrium price, we label the external effect on other purchasers a pecuniary externality because the demand and supply curves that dictate market price capture social marginal value and costs. How do we know? We have not specified any effects that are not captured by those curves: the demand curve fully accounts for the income change.

How does a non-pecuniary externality affect efficiency?

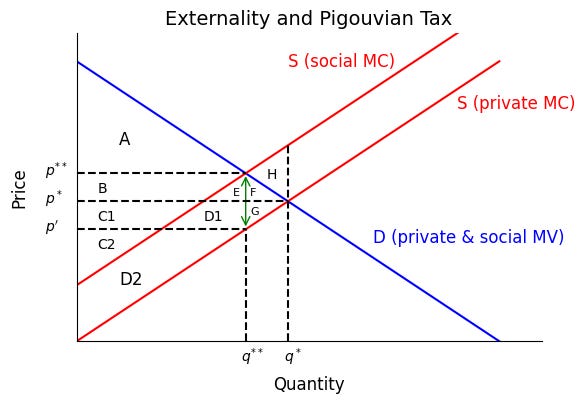

So let’s focus on non-pecuniary externalities, ones not reflected in market demand and supply curves. Consider a classical example: producers of a product like steel emit pollution from their smoke stacks and that pollution harms people living near the steel plant. The private demand curve fully captures the social marginal value of consumers of steel, none of whom, we shall assume, live near the plant. The supply curve, however, only includes the costs borne by the steel plant. It does not include the harms from pollution borne by neighbors of the plant. This means that the social supply curve lies above (higher cost) the private supply curve of market participants.

The market equilibrium is (p*,q*), the intersection of the private demand curve and the private supply curve. The efficient allocation, however, is where the social demand curve intersects the social cost curve. That is at (p**,q**). While the private and social demand are the same, the social supply curve is above the private, so the socially optimal price and quantity is lower than the private market equilibrium.

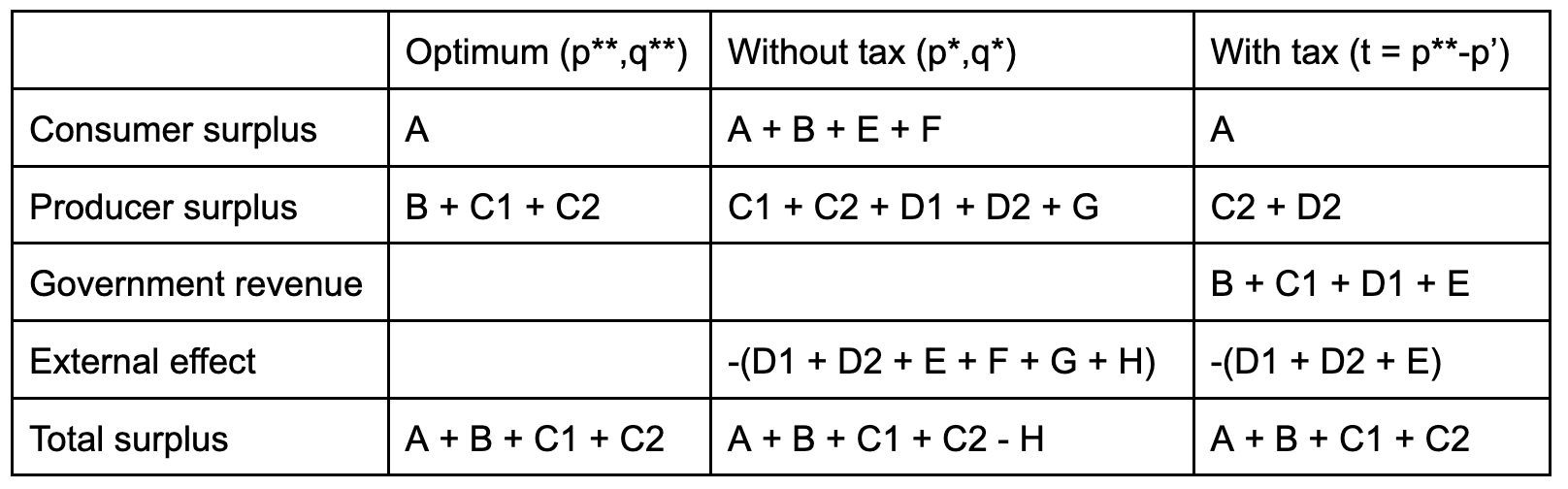

We can see how the private market equilibrium affects the social surplus and this efficiency using the table below. Consumer surplus is the area below the (private and social) demand curve and above the private market price p*: A + B + E + F. Producer surplus is the area below the price p* and above the private (not social) supply curve: C1 + C2 + D1 + D2 + G. But total surplus has to account for external effects, which equal the difference between the private and social marginal cost curves to the left of private equilibrium production q*: D1 + D2 + E + F + G + H. So the total surplus is A + B + C1 + C2 - H. We drop F + G because those are social costs, not consumer or producer surplus, respectively. Finally, we subtract H because that is quantity above the efficient amount q** where social marginal costs are greater than marginal value.

We can contrast this with social surplus when (private and) social demand equals social supply. At (p**,q**), consumer surplus is A. Producer surplus is B + C1 + C2. Total surplus is A + B + C1 + C2, which is higher than the private surplus, because the private surplus had socially excessive production, which yields a loss of H.

Query: Do the same exercise, but assume there is a positive external effect from consumption, and no negative external effect from production.

Query: Try the same exercise with positive production externalities or negative consumption externalities.

Pigouvian taxes

We have demonstrated that externalities can cause market failures. The next question is what we can do about it. One of the first proposed solutions came from the economist Alfred Pigou, who suggested imposing a tax equal to the gap between private marginal cost and social marginal cost.2 This answer is somewhat counter-intuitive because economists often say that taxes cause market failures. Yet here is a situation where taxes are advanced as a remedy for a market failure. To reconcile this seeming contradiction, let’s first explore why taxes can help fix harms from externalities. Then we’ll draw a more nuanced lesson about taxes.

Recall that an external effect causes a gap between, say, the private marginal cost of producers and the social marginal cost, which includes both costs to consumers and the externality. Suppose that we impose a tax equal to that gap, i.e., equal to the external effect. The purpose of the tax is to make the producer consider that external effect in its supply decisions.

Equilibrium with a tax is given by the quantity at which the gap between the demand curve and the supply curve is equal to the tax (and the demand curve is above the supply curve). At that point, the amount that producers want to supply at their revenue per unit (p) is equal to the amount that the consumers want to purchase at the after tax price (p + t). We learned this when we studied taxes.

Query: A quick test of your intuition: why do we need to assume the demand curve is above the supply curve?

We also learned that taxes can reduce output. When all the other assumptions about when markets are efficient hold, that is a bad thing. But what about when there are externalities, i.e., one of conditions for efficient markets is not met? Surprisingly, two wrongs can make a right.

In the figure above, we see that the quantity that causes demand to equal supply under the tax is the efficient quantity q**. Why? Because the “wedge” that our chosen tax creates is exactly equal to the difference between the private marginal cost and the social marginal cost. It makes the producer behave as if it incurs the full cost of the externality. This tax uses the fact that taxes reduce output to fix the problem that negative supply externalities cause excessive production (i.e., q* > q**).

Query: Would a tax also help address externalities not from production but from consumption, i.e., cases where social demand is less than private demand?

Query: How can subsidies help address the situation where there are positive externalities?

Showing that output under the proposed tax is equal to the efficient level of output q**, i.e., the level of output when social demand equals social supply, is our first hint that this tax can correct our externality. Let’s go further and check if surplus under the tax is the same as surplus when social demand equal social supply. Using the figure above, we see that at the optimum allocation consumer surplus would be A (below social/private demand, above p**) and producer surplus would be B + C1 + C2 (below p**, above social supply), so that total surplus is A + B + C1 + C2. When there is no tax, the consumer surplus is A + B + E + F (below social/private demand, above p*) and producer surplus would be C1 + D1 + G + C2 + D2 (below p*, above private supply). Now, with tax, quantity is q**, producers get p’, and consumers pay p’ + t = p**. So consumer surplus is A (private/social demand - p**), producer surplus is C2 + D2, tax revenue is B + E + C1 + D1, and external costs are D1 + D2 + E. Total surplus is consumer surplus, plus producer surplus, plus tax revenue, minus external costs, or A + B + C1 + C2. That is greater than surplus without the tax, and the same as the surplus at the optimum.3

We have now shown that taxes can help fix externalities. But that does not mean that taxes are always good. Without an externality, taxes can still lead to inefficiently low output. So we need to be more nuanced in our analysis of taxes. To help, we often distinguish taxes that correct externalities as Pigouvian taxes, after the economist that showed they could correct for externalities. And other taxes as plain taxes.

Alternative tools to address externalities

Pigou kicked off a long debate over how to address externalities. His solution was to manipulate prices via taxes (or subsidies). But there are other solutions. A related solution is quantity restrictions.4 Specifically, if one could limit quantity to q**, you would get the optimal quantity. Price would be determined by bargaining between producers and consumers. If there were a single producer, the per-unit revenue of the supplier would be p**, and the area B + C1 + D1 + E would go to the producer rather than the government. Consumer surplus would be the same as with the tax, since the price buyers would pay would be p**. And the external effect would remain the same as with a tax (D1 + D2 + E) since quantity would be the same as under the tax. The total surplus is the same as with the tax.

Other economists, especially Ronald Coase, had doubts about these solutions. He felt that the government could not accurately estimate either the externality (thus the tax), let alone the externality, demand curve and supply curve (thus the optimal quantity restriction). He worried the government did not have enough information to make good decisions. They might over or under correct for the externality. He thought a better solution was to give private parties with the relevant information an incentive to get the efficient outcome. Specifically, he suggested that the government modify property rights to fix these incentives. For example, the government could give neighbors of the steel mill the right to be free from pollution. Then, they could sue the steel mill to compensate them for their injuries. That litigation would cause the steel mill to consider the cost of its externality when deciding how much steel to produce and thus pollution to emit.5 We will return to this solution when we discuss property law, and also when we discuss tort law.

If the legal rule change or the change in social norms also affects your preferences such that, in 1960 you did not dislike my smoking and today you do, then the external effect would change too. But the science tells us that the health impact of my smoking on you has not changed over time. And if you cared about health effects, you would object to my smoking even is the law and norms did not.

From Claude.ai: Arthur Cecil Pigou was a British economist who taught at Cambridge University from 1908 to 1943 and made fundamental contributions to welfare economics. His most significant insight was the concept of externalities - costs or benefits that affect third parties not directly involved in a transaction. He argued that government intervention through taxes (now called "Pigovian taxes") could correct market failures by forcing companies to account for the social costs of their activities, like pollution. His 1920 book "The Economics of Welfare" established the theoretical foundation for environmental economics and government regulation of markets. Pigou was also an early advocate for unemployment insurance and progressive taxation. A lifelong bachelor, he lived relatively solitary, dedicating himself to academics and mountaineering in the Alps during summers. During WWI, he served as a civilian porter in France after being rejected from military service, demonstrating his commitment to supporting the war effort despite his pacifist beliefs.

The main difference between the social optimum and the tax is that, instead of the producer getting B + C1 + C2, the government gets the B + C1 portion and the producer gets only the C2 portion. What should we do about this? If we care only about efficiency, nothing. But if we care about producers, or political lobbying against the tax by producers, we can transfer B + C1 to producers. But we can’t make it a subsidy for production, i.e., proportional to output, otherwise we would undo our tax and get our externality back. We have to give the B + C1 back in a way that producers think is not tied to output. Economists sometimes say “give it to them as a lump sum”. Implementing this is much harder.

Martin Weitzman is associated with using quantity restrictions to address externalities. Here is Claude.ai on Weitzman: “Martin Weitzman (1942-2019) was a Harvard economist who made pioneering contributions to environmental economics and the economics of catastrophic risks. His work on uncertainty and climate change, particularly his "Dismal Theorem," demonstrated how standard cost-benefit analysis breaks down when facing potentially infinite damages. Building on Pigou's work on externalities, he developed influential theories on optimal environmental regulation, comparing price (carbon taxes) versus quantity (cap-and-trade) instruments. His "Share Economy" theory also proposed innovative solutions to unemployment and inflation.”

If transaction costs (including collective action problems or hold-up risks) were zero, i.e., the cost of the steel company buying the right to pollute from neighbors was non-trivial, then it would not even matter who got property rights over the air quality. If the steel company had the right to pollute, the neighbors could buy it from the steel company, an opportunity that the steel company would consider a cost when it produced steel because producing more steel meant that the neighbors would not pay for as much clean air.